SMM June 30 Report:

As of June 30, the most-traded SHFE zinc contract closed at 22,495 yuan/mt, up 270 yuan/mt month-on-month, with a decline of 1.21%. In June, zinc prices first fell and then rose, hitting a low of 21,660 yuan/mt in mid-month before rebounding to a high of 22,570 yuan/mt at the end of the month. As we enter July, how will zinc prices perform?

Macro Perspective. In June, geopolitical risks increased, and trade prospects became more uncertain, but these risks later subsided. Additionally, US economic data was weak, and the US dollar index and US Treasury yields pulled back, boosting expectations for US Fed interest rate cuts. The phone call between the Chinese and US presidents brought optimistic market expectations. Meanwhile, the central bank's trillion-yuan reverse repo operations signaled a clear intention to boost domestic demand by releasing liquidity. At the same time, during the Shanghai Lujiazui Forum in China, the central bank introduced eight policy measures to support the construction of Shanghai as an international financial center, with monetary policy as the main focus, creating a generally positive macro sentiment. As we enter July, geopolitical tensions still persist, and US economic data remains weak, reigniting market expectations for interest rate cuts.

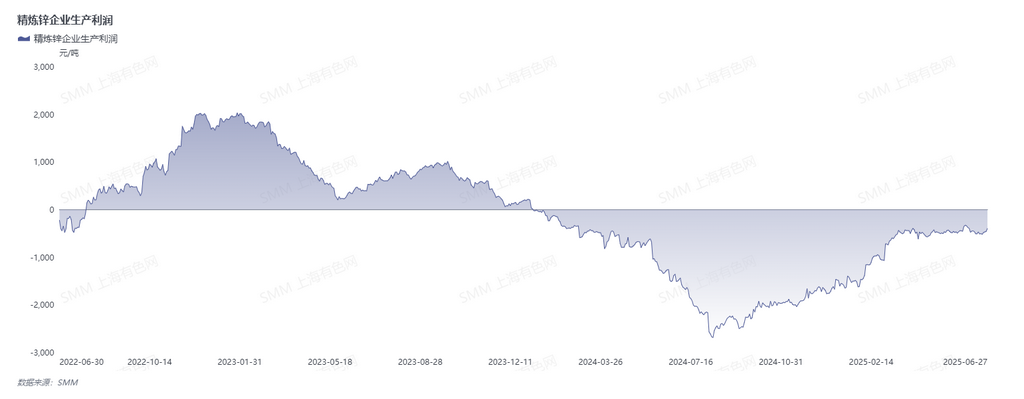

Supply Side. With the continuous release of new capacity at smelters and the gradual resumption of maintenance enterprises, coupled with the arrival of the rainy season in some regions, electricity costs have decreased. Enterprises, enjoying high profits from sulphuric acid and minor metals on a YoY basis, have high production enthusiasm. The trend of increased refined zinc production continues. Although imports of zinc ingots and zinc concentrates decreased in May, zinc concentrate imports were still at a high level, up 84.26% YoY, indicating a relatively loose supply, but the increase was less than expected. As we enter July, with the concentrated arrivals of imported ore in the previous period, smelters' raw material inventories are relatively loose. Although some large smelters will undergo maintenance in July, TCs continue to rise, and production profits for refined zinc enterprises are good. Additionally, some new zinc ingot capacity will be gradually released in July. It is expected that the overall zinc ingot supply level will remain strong in July.

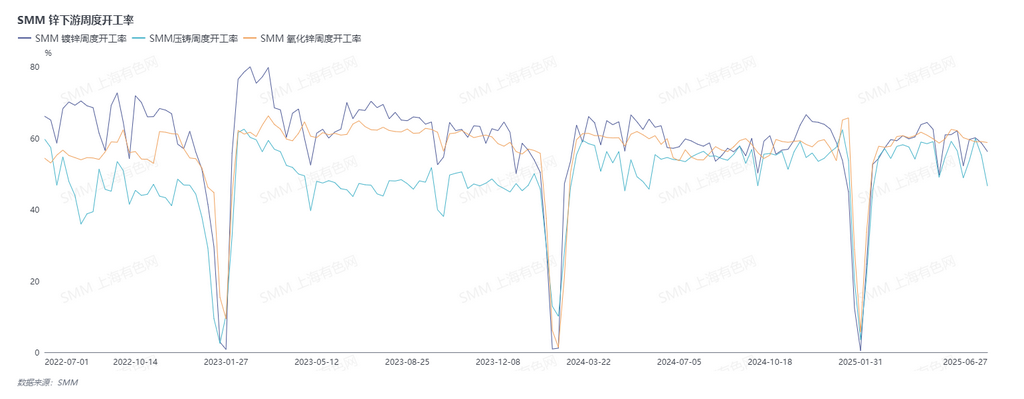

Demand Side. In June, as temperatures gradually rose and the plum rain season approached, infrastructure project construction was limited, and orders across various terminal sectors declined. Previous export orders were also continuously digested, and domestic demand was weak. Overall, downstream zinc consumption gradually decreased in June. As we enter July, the third batch of funds for the trade-in policy for consumer goods will be disbursed in July. Relevant departments will formulate monthly and weekly "national subsidy" fund usage plans for different fields to ensure the orderly implementation of the trade-in policy for consumer goods throughout the year. However, with the increase in high-temperature weather and frequent heavy rainfall, terminal construction is limited. It is expected that demand may decline in July, and zinc consumption will gradually weaken.

Looking ahead to July, the domestic market shows a pattern of strong supply and weak demand on the fundamentals side. Zinc ingot production is increasing, and it is expected that social inventory of zinc ingots may start to build up, putting pressure on zinc prices. However, there are many disturbances in overseas fundamentals. Zinc demand in Southeast Asian countries is good, and LME inventory continues to destock to a low level, indicating strong overseas demand that may support zinc prices. It is necessary to continuously monitor subsequent macro guidance and overseas fundamental performance.

(The above information is based on market collection and comprehensive assessment by the SMM research team. The information provided herein is for reference only. This article does not constitute direct advice for investment research decisions. Customers should make cautious decisions and should not replace their independent judgment with this information. Any decisions made by customers are not related to SMM.)